Louis Wheeler

Casino stocks are always on the house. That's according to savvy investors who have been monitoring the performance of casino stocks over the years. Top-performing casinos are gearing up to reward investors with handsome dividends in the near future.

For example, Wynn Resorts Ltd (WYNN). The company has prospered thanks to the performance of its Las Vegas operations, Wynn Macau, and Wynn Palace.

Given that Wynn Resorts Ltd generates the lion’s share of its revenue from its Asian operations in Macau, there is a degree of trepidation among investors whether the ongoing trade war between the United States and China will impact profitability for the company.

The company focuses on a multi-pronged strategy which includes driving up revenues through non-gaming activity vis-a-vis entertainment, accommodation, wining and dining, and general tourism. This diversification strategy is already paying dividends for the group, in tandem with robust gambling revenues in Macau.

One of the biggest drivers of success for this top-performing casino stock is Cotai, Macau. This resort is slated to enjoy a massive boost in tourism numbers and casual gambling in the future. The Wynn Group is anticipating large-scale tourism across multiple regions, notably a pair of new restaurants in Las Vegas, new resorts in Boston (Encore Boston Harbor), and a complete redesign of Wynn Macau, among others.

Naturally, there is room for growth with the company, particularly property prices in China. Since the company is heavily reliant on debt financing, a trade war between the two superpowers could adversely affect the bottom line. By Q2 2019, Wynn Resorts Ltd owed $9.15 billion. Owing to its high debt burden, the company faces difficulties in respect of financing new projects.

Wynn Resorts Ltd (WYNN: NASDAQ) is trading around $105.88 per share (August 19, 2019), with a market capitalization of $11.031 billion and an EPS (earnings per share) of $4.00. The company has a dividend yield of 3.90% and a price/earnings ratio of 25.72.

The rollercoaster performance of WYNN stock in 2019 mirrors the concerns related to the US/China trade debacle. The stock hit $149 in April, collapsed spectacularly to approximately $104, before rising towards $140 in late July. The current stock price is reflective of overall market volatility, especially as it pertains to China.

Over the past 5 years, the stock has come under significant pressure but bounced back spectacularly well. A protracted boom period between September 2015 and May 2018 resulted in significant gains as the price of the stock climbed towards $200 per share. Analysts point to the long-term bullish trend since inception in 2003 when WYNN was trading at around $12.85 a share. Viewed in perspective, there has been a 740.13% increase in value since that time.

WYNN is an overall great casino stock to own. It is rightfully on our best casino stocks list, thanks to a spectacular run of form over the years. It would be foolhardy to recommend a massive investment at this time, given that markets look like they are plunging down the rollercoaster tracks at breakneck speed.

If you own the stock, hold it, it's likely to reverse at some point. If you’re looking to buy this casino stock, do so incrementally so that you can get the best dollar-cost averaging for your money. It has already proven itself to be a strong performer, and it's currently trading at two thirds of its 52-week price range.

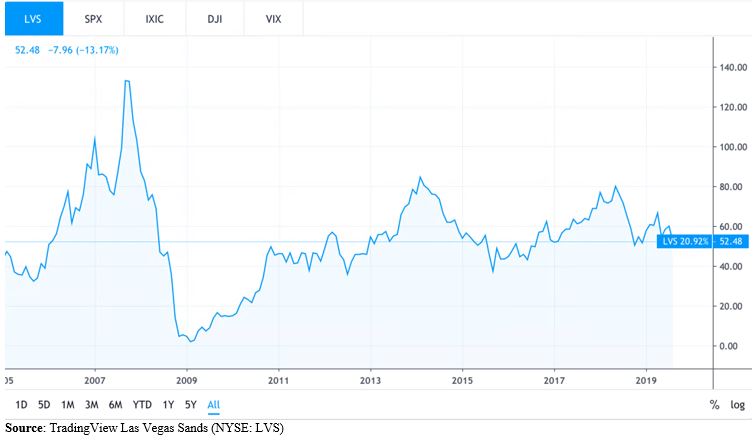

The Las Vegas Sands Corporation is listed on the New York Stock Exchange. At the time of writing, the stock was trading at $52.48 per share, with a 52-week low of $47.39 and a 52-week high of $69.60 per share. With a market capitalization of $40.425 billion and $2.48 EPS, LVS is regarded as a fair value buy option. The recent performance of the company has been lacklustre, given multiple earnings misses in Q3 2018, Q4 2018, and Q2 2019.

In Q1 2019, LVS surprised analysts with an earnings beat ($0.04), helping to boost the performance of the stock heading into the second half of the year. With growing concerns about US and China trade relations, the stock has plateaued. The 1-year target estimate price of LVS is $70.72, indicating significant optimism among traders and investors.

Since it was listed in 2005, LVS has generated returns of 20.92% overall, significantly shy of WYNN, but positive nonetheless. The trading chart for LVS offers a unique insight into the performance of the stock since the global financial crisis. It has recovered well and maintained a solid share price despite multiple geopolitical shocks. It is a stable stock with strong potential.

A Kiplinger article by Charles Lewis Sizemore highlighted the strength of the Las Vegas Sands. The company is a worldwide leader in integrated resort development and operation. It owns an impressive portfolio of assets (hotels, casinos, and resorts) across the world, including the Four Seasons Hotel Macao, The Venetian Macao Resort Hotel, The Venetian Resort Hotel Casino on the Las Vegas Strip, the Plaza Macao and others.

Much like its competition, Wynn Resorts Limited (WYNN), LVS is currently being hamstrung by its deep ties to China. Consider that an estimated 61% of the company’s earnings (EBITDA) were derived from Macao, 27% from Singapore, and just 12% from the US.

While the fundamentals of the stock are strong, and the portfolio of investments under the umbrella of the Las Vegas Sands is substantial, the trade war between the US and China is a real source of concern.

This stock has strong growth prospects. It is hovering close to its 52-week low of $47.39, so it's best to keep this one on the watchlist. If you're thinking of buying this casino stock, expect volatility for some time. Ultimately, the fundamentals are good.

888 Holdings plc is listed on the London Stock Exchange (LSE). The share price is 146.40 GBp, with a 52-week high of 239.00 and a 52-week low of 126.70. The company's financial statements (2018-12-31) over six months indicate revenue of $256.7 million, with total operating expenses of $217 million and operating income of $39.7 million. The net income before taxes was measured at $48.6 million and $39.4 million after taxes.

The company has 68 institutional shareholders owning 39.34% of all shares. Casino revenues for the year ending December 31, 2018 amounted to $317.6 million, poker $49.0 million, sport $80.3 million, and bingo $32.4 billion. The total of business to consumer business (B2C) activity amounted to $479.3 million, with business to business (B2B) operations generating $50.6 million.

888 Holdings plc manages multiple verticals, including bingo, poker, casino, sports betting, games, B2B, B2C and other operations. Its flagship casino brand is 888casino, a global leader in the online casino and gaming industry. 888casino offers games such as roulette, slots, blackjack and more.

With 25 million+ registered players at the casino, 10 million+ players at the poker room, and millions more in the wings, this online gaming juggernaut certainly has the numbers to generate the profits. Recent overhauls of the gaming platforms on poker (Poker 8), and casino (Orbit) have thrust the 888 Group into the limelight as industry leaders in the online gaming realm.

This one certainly qualifies for one of the best casino stock in 2020, for several reasons. 888 has invested in the rebranding and redesign of many of its flagship verticals. It is currently fully licensed and regulated to offer real-money gambling games to players in New Jersey (NJDGE), the United Kingdom (UKGC), Malta (MGA), Ireland (Ireland Revenue Commissioners), and Gibraltar (Government of Gibraltar) with negotiations currently underway for licensing in other markets.

Recommendation ratings for 888 indicate a majority of analysts favouring a strong buy or a buy rating, with a minority hold rating on the stock. Revenue and earnings have been consistent over the years, with 2017 and 2018 earnings approaching $550 million. In 2018, earnings increased substantially towards the $100 million mark. The company's market capitalization is an impressive $538.54 million with a 25.80 EPS, and a 1-year target estimate price of 2.76.

This LSE-listed public company has positioned itself well, given fears of a Brexit. It is on the FTSE 250 index, yet it has licenses in multiple jurisdictions to allow players to enjoy regulated gaming all over the world. This should protect it against Brexit shocks.

The stock is affordably priced at £1.4640, making it ideal for new investors looking to cash in on a low-cost, yet valuable casino stock. The year-to-date performance has mirrored that of many other casino stocks, yet the past several months for 888 Holdings plc have been bullish.

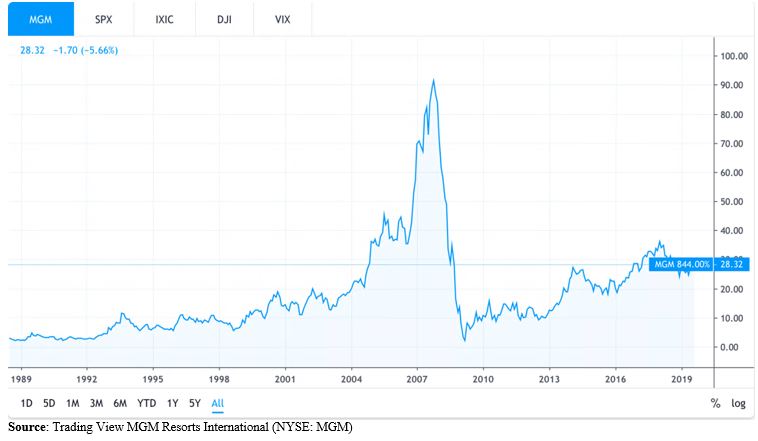

MGM Resorts International (MGM) is currently trading at $28.32 per share, with a $14.563 billion market capitalization, and a 1.86% dividend yield. The stock has paid $0.34 earnings per share, with a price/earnings ratio of 83.58. If you're wondering which casino stocks to buy you may be tempted to invest in MGM.

Our analysts studied the performance of this stock and found that it is currently overvalued. The price-earnings ratio of 84.04 is significantly higher than the competition indicating that the stock’s price is high relative to its earnings. For the year to date, the stock has maintained value, with little whipsaw activity up or down. The 1-year target estimate price is $33.56 per share ($5.24 higher than the current price, or an 18.5% premium).

MGM enjoys heavy trading volume, which is typically a good thing. This indicates there is interest in the stock. On the downside, MGM consensus EPS (earnings per share) has consistently fallen short of actual earnings per share in Q4 2018, Q1 2019, and Q2 2019. This indicates less than optimal performance, despite sentiment. On a rating scale of 1-5, where 1 represents a strong buy and 5 represents a sell, the stock ranks at 2.3.

Of the last six upgrades & downgrades, 2 have been downgrades and 4 have been maintains. The absence of upgraded rankings indicates scant optimism about the stock in 2019. Does this mean it shouldn't be on the best casino stocks 2019 list? Absolutely not – MGM certainly has some challenges but many of them are related to the current concerns with China.

MGM stock is currently trending bearish. The 30-day high of the stock was $31.68, and the 30-day low was $27.59. Over the past 90 days, the stock bottomed out at $23.68, and topped out at $31.68. The stock is trending bullish over the long term. Current support levels for the stock appear to be holding at $27.74 and resistance levels above $28.90 remain strong.

Given that it is a relatively low-risk proposition, one has to evaluate it on its merits. For this, we go to our technical indicators. The 50-day moving average of the stock is $28.60 (above the current price), and the 200-day moving average is $26.99 (below the current price). This indicates cautious optimism for MGM stock buyers. Given this data, a hold rating is the best option.

With digital marketing strategies in his blood, Louis Wheeler has traveled around the world, exploring gambling cultures and gaining experience in casino games from 2003. If you are in a casino anywhere around the planet, you may find him right next to you, playing blackjack, roulette or texas hold'em.